Case Studies

Selected work across tequila, agave research, brand development, and creative strategy.

Case Study

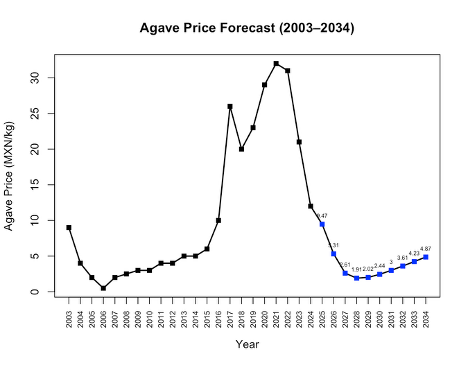

Agave Price Forecast

This forecast analyzes historical agave prices alongside projected tequila production growth to estimate future price movement from 2025 to 2034. After the major agave price spike between 2017 and 2022, the model projects a sharp correction followed by gradual price recovery later in the forecast period.

The analysis helps identify potential sourcing risks, cost exposure, and long-term market pressure within the tequila supply chain.

- Shows historical agave prices from 2003–2024

- Projects possible agave prices from 2025–2034

- Uses past price behavior and tequila production growth as forecasting inputs

- Assumes tequila production continues growing at approximately 3% per year

- Supports planning around sourcing, cost exposure, and future market pressure

Forecasted Agave Price

| Year | Forecasted Price MXN/KG |

|---|---|

| 2025 | 9.470631 |

| 2026 | 5.310221 |

| 2027 | 2.605933 |

| 2028 | 1.909590 |

| 2029 | 2.015990 |

| 2030 | 2.443314 |

| 2031 | 2.998939 |

| 2032 | 3.605857 |

| 2033 | 4.233280 |

| 2034 | 4.868901 |

Case Study

Tequila Market Structure

Tequila is one of the fastest-growing spirits categories in the world. The U.S. market has expanded by more than 300% since 2003, demand continues to climb, and the category generates a disproportionate share of total spirits revenue relative to its volume. By most measures, the opportunity has never been larger.

But aggregate growth tells an incomplete story. The United States absorbs over 82% of all tequila exports by volume, making U.S. distribution access not just advantageous but effectively determinative of whether a brand can compete internationally at all. Within that market, four multinational parent companies — Diageo, Proximo Spirits, Bacardi, and Beam Suntory — collectively control nearly two-thirds of both dollar and volume sales. Their advantage is not only brand recognition. It is distribution infrastructure, capital access, portfolio strategy, and market visibility operating at a scale smaller producers cannot easily match.

The premium segment compounds the imbalance further. Nearly half of all retail tequila dollars are spent on bottles priced at $45 and above, and luxury tequila grew at an average of 37% annually between 2018 and 2023 — the fastest rate of any spirits category tracked in the period. The segment generating the most revenue per bottle is also the segment most dependent on brand investment, distributor relationships, and on-premise visibility — precisely the resources that are hardest for independent and emerging producers to access.

At the same time, international markets remain open. Outside the United States, tequila is still developing its position in many premium beverage markets, creating room for brands that can enter early, educate the trade, and build credibility before the category becomes fully consolidated. For smaller producers, the opportunity is not necessarily to outspend the largest companies, but to identify markets where timing, positioning, relationships, and cultural fluency can still create an advantage.

For smaller brands and independent producers, this is the environment they are entering. The market is large and growing, the consumer appetite for premium and craft expressions is real, and the structural barriers to capturing that demand are significant. Navigating them requires a clear understanding of where the category is going, who controls the channels that matter, and how to position a brand to compete on the terms where size is not the only advantage.

That is the work.